Best Way to Finance a House for Low Income Families

Low Income Dwelling Loan Options Requite You Hope

Cheers to the many depression-income dwelling house loans bachelor today, y'all can be a homeowner even if y'all don't make a lot of money.

In this commodity, my goal is to requite you lot all the tools you need to detect, utilise for, and successfully close on a mortgage loan despite having a low income.

These loans will requite y'all hope you can buy a home without saving 10% to 20% of the domicile's price for a downwardly payment. And more important, hope y'all can afford the monthly payment once you move in.

Click here to encounter if you are eligible to buy a home.

In this article:

- Low-income dwelling loan options

- Downpayment assistance

- Grants for low-income families

- Seller-paid closing costs

- How lenders decide to approve your loan

- Our recommended lenders for low-income loans

The All-time Depression-Income Mortgage Options

Edifice a house takes a well-stocked tool belt, and so does buying one. Here are some of the best low-income mortgage options.

Finding the correct home loan for a lower budget is a process but it's one worth undertaking. Discovering these depression-income home loan types might exist just the get-go step. See Part 2 of this article about how lenders decide whether you're approved for the loan. Your next steps may exist to work on your credit or savings habits to make your loan app look that much meliorate. For now, let's get correct to the specific habitation loan programs.

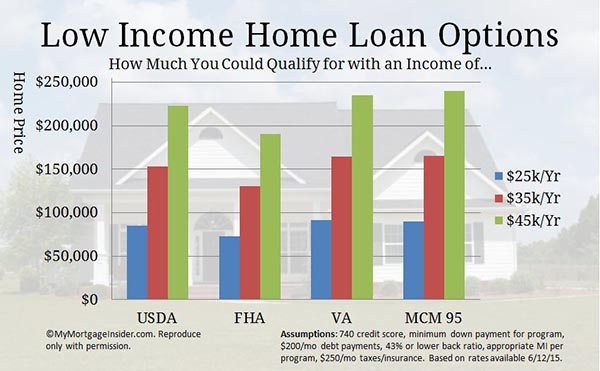

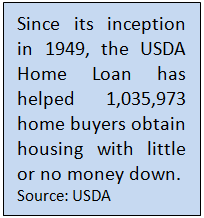

USDA Dwelling house Loan: Nix-downwardly Loan Option

The USDA loan lets yous purchase a dwelling house with nil downwardly payment. It's available for properties in areas the USDA designates as rural, although many eligible areas are quite suburban. To check out eligible areas, run across USDA'southward property eligibility map.

This programme is too called the Rural Evolution loan or USDA Guaranteed Loan programme. It has been a fantastic dwelling house loan for low-income families over the years. You can buy a domicile at a low-interest charge per unit with little or nothing out of pocket.

What'due south more than, the USDA loan is specifically designed for

What'due south more than, the USDA loan is specifically designed for

- People who don't already own an adequate home.

- Those who brand 115% or less of the expanse's median income.

Click here to check your USDA abode loan eligibility.

USDA Low Income Loan (USDA Direct Loan)

This program is prepare specifically every bit a dwelling loan for low-income families. Also known as Department 502 loans, they are available to individuals with very low and depression incomes, defined as 50% to 80% of the area's median income.

You lot can have a 33-year term or fifty-fifty a 38-year term in some cases. And, payment subsidies are bachelor for those who don't qualify for the full payment.

To see if your income is within limits, see USDA's Direct Loan income limits page.

Keep in mind standard domicile loan lenders exercise not offering this program. You lot take to apply through USDA direct.

Your income must be too low for other loan programs to be eligible. You have to make sure yous don't qualify for a standard USDA loan before you utilise for a USDA direct loan.

Speak to a USDA loan professional virtually standard USDA financing by completing a brusk questionnaire here.

FHA Loan: A Great Mortgage Option for Lower Incomes

You lot've probably already heard of the FHA loan plan. It's another regime-backed loan type that helps depression-income individuals purchase a dwelling. Here are the highlights of this program:

- 3.5% down payment

- The seller can pay all or most of your endmost costs

- Allows lower credit scores than conventional financing

As a low-income home buyer, hither are some additional features of an FHA loan that you will exist interested in:

- The 3.v% downward payment can come up from downwardly payment souvenir coin.

- FHA has more lenient debt ratio requirements than conventional financing, meaning y'all might qualify with a lower income.

- FHA does non require you to have the actress coin in the bank afterward endmost the loan.

- You can use a co-signer (another political party who contributes to the loan repayment but won't live in the home).

FHA is designed with low-income families in mind. It has helped millions break into homeownership despite traditional barriers.

Click here to see if you lot qualify for an FHA loan now.

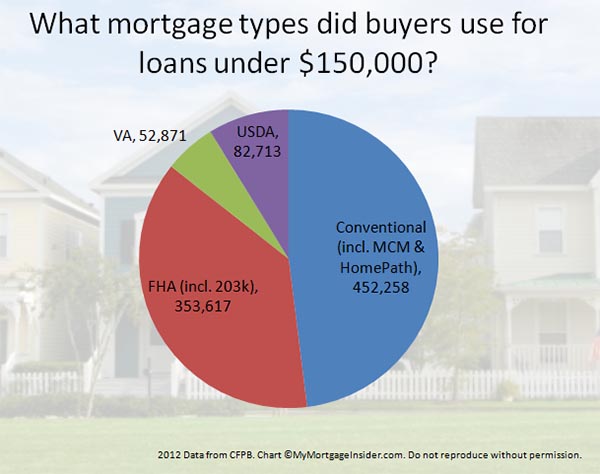

FHA 203k: Purchase and Fix Up a Home with 1 Loan

An FHA 203k loan is basically an FHA loan with an added characteristic: the ability to finance the purchase price and rehab costs into the mortgage.

This loan program is ane of the best low-income home loans because it lets take advantage of lower prices on fixer-uppers.

At the end of this article, I talk near how the lender makes sure the property meets minimum standards. Well, with an FHA 203k, that doesn't matter. You finance the repairs needed to bring it upward to FHA's minimum property requirements.

Because the homes don't meet the requirements for traditional financing, they are typically steeply discounted. This allows those with a lower income to get into a home more easily.

Click here to check your FHA eligibility now.

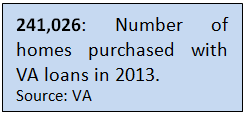

VA Mortgage: The Cheapest Monthly Mortgage Payments

If y'all accept war machine feel, the VA mortgage should be the first depression-income mortgage option y'all check out. Information technology requires null downward payment and the seller tin can pay all or almost of your closing costs.

There'southward no monthly mortgage insurance and that tin can save y'all hundreds per month. No mortgage insurance means you tin buy more than abode with less monthly income compared to other loan types.

There'southward no monthly mortgage insurance and that tin can save y'all hundreds per month. No mortgage insurance means you tin buy more than abode with less monthly income compared to other loan types.

And, VA loans are more than lenient on debt ratio and credit score requirements. Many low-income individuals and families have used a VA loan to buy their showtime abode.

To be eligible, you must take United states military service feel of at to the lowest degree

- ninety days or more than in wartime if currently on active duty

- 181 days or more in peacetime

- 24 months or the full menstruation for which you were ordered, if at present separated from service.

- 6 years, if in the National Baby-sit or Reserves

If you are eligible, you could be very close to owning your own home despite currently being on a low income.

Click here to check your VA home loan eligibility.

HomePath and HomePath Renovation Dwelling house Loans – Fannie Mae's Foreclosed Homes

Editor's note: Fannie Mae ended their HomePath program on Oct six, 2014. For more details, visit our Fannie Mae HomePath page.

The HomePath programme allows low-income habitation buyers to authorize more hands than almost other loan programs. Here are a few of the cracking things about HomePath:

- Only 5% down payment required

- No appraisal required

- No minimum property standards to run into

- No private mortgage insurance required.

This loan could help you lot buy a fixer-upper at a low toll. Your monthly payment will fit into your budget much easier than many homes that are in top shape. And no mortgage insurance means a big reduction in your monthly costs.

These homes are Fannie Mae-endemic foreclosures. Fannie's goal is to sell these homes to great potential homeowners like you. And then, they remove many of the traditional roadblocks to owning a dwelling house like PMI and a large down payment.

That'southward keen news for buyers looking for a low income mortgage. Notice a list of homes for sale in your area by searching on HomePath.com. Then call an approved HomePath lender here and get started.

There's as well an option to purchase and repair the home with a HomePath Renovation loan. You can buy and fix up the property to your liking, using just 1 loan.

See complete HomePath guidelines here and HomePath Renovation guidelines hither.

HomeReady 3% Downward Mortgage

The new HomeReady program from Fannie Mae is extremely flexible on sources of income. Applicants tin can use the income of household members who are non on the loan as a compensating gene. That means a family fellow member who does not want to be on the loan tin however help you qualify.

In addition, you lot can utilise boarder and roommate income, rental income from a basement apartment, and non-occupant co-borrower income to qualify.

The downwardly payment requirement is just iii% and can come entirely from a souvenir or canonical down payment assistance program.

Meet if yous can buy a dwelling house with the HomeReady mortgage program.

Good Neighbour Next Door – Homes Discounted 50%. Simply a $100 Downwardly Payment Needed

The Skilful Neighbor Next Door (GNND) program is a special loan type offered past the United states Department of Housing and Urban Development (HUD). It allows police enforcement officers, teachers and emergency personnel to purchase homes at a 50% discount!

Hither'due south how it works. Y'all find a home on HUD's GNND website and brand an offer. If more than than i person submits an offer, a random lottery is held to see whose offer is accustomed.

If you are selected, y'all must prove that y'all are an canonical type of public worker.

HUD establishes a "silent 2d" mortgage for l% of the listed price. But if you live in the home for a full iii years, that debt is erased!

You can apply diverse types of financing for this programme. But if yous use FHA, your down payment requirement is merely $100.

If you meet the in a higher place criteria, this is a perfect depression-income mortgage option. After all, you just take to make payments on 50% of the dwelling'south purchase price. Contact one of our loan professionals here to check involvement rates and go started.

Manufactured Housing: Mobile Dwelling house Loans

Manufactured homes represent a big part of available homes in many areas. You tin discover some actually depression prices on manufactured homes, usually chosen mobile homes.

Mobile homes can be a great way to get into a dwelling for much less money upfront and monthly. They don't appreciate the same way standard stick-built unmarried-family homes exercise. Still, they can exist a not bad fashion to break into homeownership.

Just be certain that yous simply await at homes built on or after June 15, 1976. Any mobile home congenital prior to this date can't exist financed with any traditional loan.

Click here to run into if yous qualify to purchase a manufactured abode.

An FHA loan is the easiest fashion to finance a mobile abode purchase. Standard FHA rules apply, similar iii.5% downward and lower credit standards, but there are some additional property inspections required.

To meet complete guidelines on FHA loans for mobile home, bank check out our blog post or only click hither to meet if you qualify to buy a manufactured home.

Down Payment Assistance from Charitable & Regime Organizations

Y'all'd be surprised at how many cities, counties, states, offer down payment help to low and moderate-income home buyers. In fact, at that place are too many to list.

Downward payment assistance, otherwise known every bit DPA, is a powerful tool for homeownership. It eliminates years of scrimping and saving for a down payment. When you accept a low income, information technology's tough to salve plenty to buy a home.

HUD'south HOME Investment Partnership Program

HUD distributes funds each year to jurisdictions in all 50 states to help low-income home buyers. Eligible buyers must make no more than eighty% of the expanse'southward median income.

Jurisdictions that administrate the funds are too many to list, but you can easily find out if there is a HOME-sponsored program in your area here.

DPA funds can be used in combination with many standard loan types. If there is a program in your area, contact a knowledgeable loan officer to see if y'all can combine downward payment help with the loan type you're interested in.

Click here to check your homebuying eligibility.

Downwardly Payment Assistance from Cities, States, and Counties

Many local governments offer DPA funds to lower-income borrowers. Down payment assistance programs revitalize urban and suburban areas. It encourages families to buy homes, motility in, and ameliorate the customs.

Many local governments offer DPA funds to lower-income borrowers. Down payment assistance programs revitalize urban and suburban areas. It encourages families to buy homes, motility in, and ameliorate the customs.

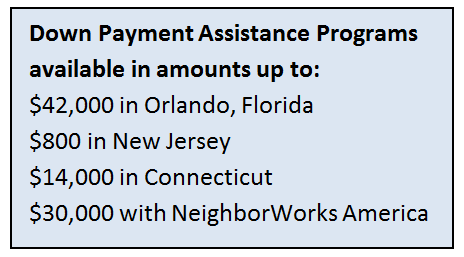

Hither are some examples of down payment assist bachelor:

- Orlando, Florida: $42,000

- New Jersey: $800

- Connecticut: $14,000

- Seattle: $45,000

- St. Louis, Missouri: $5,000

Each programme is a little different. Sometimes the down payment assistance is a depression-income grant that yous don't accept to repay. Other DPA programs lend you money at little or no interest just demand to be repaid somewhen.

Inquire a local real manor agent about down payment assistance programs in your area, and see our folio downwardly payment assistance page for more examples of organizations that participate.

Charitable Organizations

Some charitable organizations are able to contribute down payment assistance funds toward FHA loans. Just, they must be approved by HUD.

To run into if a non-regime system in your area is approved search by name or location hither.

Click hither to come across which downwards payment assistance programs are available to you.

Grants for Low-Income Families to Buy a House

All beyond the state, there are city-, canton-, and land-based grant programs to aid depression-income families to purchase a house.

And I'g going to tell y'all how to detect them.

Housing is getting expensive, especially in major metros. That'due south why local governments are getting involved in downwards payment and closing cost assist.

Many locales tin't bring home prices downward in their region. Only what they can do is give away money to help families get into homes when they otherwise couldn't.

Unfortunately, there are non many, if any, centralized databases of all these individual grant programs. Each grant has its own rules, dollar amounts, and geographic restrictions.

But you tin can find these programs with something you lot utilize all the time anyhow: Google.

Check this out.

Merely Google your city, state, or canton name followed by "housing grant". In near 3 minutes, I was able to find very good programs in Seattle, Miami, North Dakota, Connecticut, and Clark County, Nevada.

Literally, every location I Googled had a housing program.

Here's a sample of what I plant:

- Seattle: Up to $55,000 (yep, that much) in down payment assistance to families earning less than eighty% of the expanse median income.

- Miami: ii% of the abode price for low- and moderate-income families

- North Dakota: Just $500 out of pocket to buy. Offset-time home buyers who see income requirements are eligible.

- Connecticut: Full downwardly payment covered (typically 3-3.5%) via a low-interest loan.

- Clark Canton, Nevada: A non-repayable grant of 4% of the loan amount to cover down payment and endmost costs.

These are just a few of the hundreds of grant programs available beyond the country for low-income families. With simply a few minutes of enquiry, you could exist on your fashion to homeownership through a grant program.

More than About Low-Income Mortgage Options

The government wants y'all to go a low-income mortgage.

Information technology sounds strange, but really, it'southward not.

Co-ordinate to the National Association of Domicile Builders, homeownership makes upwardly about 15% to 18% of the U.S. economy. Without homeowners, economic growth would simply finish.

So, the government sponsors a myriad of programs — FHA, USDA, VA loans, plus many conventional programs — to spur homeownership among average and fifty-fifty beneath average wage earners.

Due to these programs, information technology'southward non uncommon for waitresses, factory workers, and even seasonal workers to go depression-income mortgages.

The problem is, many renters continue to hire because they assume they can't qualify.

They don't realize they can request a pre-approval with a lender, typically for just the cost of a credit report, and the lender might even choice up the tab for that.

The point is, a low-income mortgage is inside reach to many thousands of lower-wage earners in cities across the U.Due south. — but it's upwards to them to bank check their eligibility.

Ready to see if you're eligible? Get started here.

Seller-Paid Closing Costs Help With Your Low-Income Mortgage

When looking for low-income mortgage loans, you'll want to consider the total cost of getting into a home, which includes the downward payment plus the loan endmost costs.

A bang-up fashion to reduce costs is getting the seller to pay your closing costs. Closing costs can be several g dollars which could put a real hamper on your home buying aspirations.

Why would the seller pay your endmost costs? Considering the current owner of the abode wants to sell the domicile, probably almost as much as yous desire to buy it. Many homeowners or banks (if the home is a foreclosure) give the buyer thousands of dollars to ensure a smooth closing.

Work with your real manor amanuensis to go about asking for closing costs properly. You lot'll need to ask for the right amount for the situation.

If the home y'all are looking at has multiple offers, they probably won't accept one that is asking for closing cost help.

Yous may want to look at homes that need work or are in less demand. Sellers are unremarkably more willing to pay closing costs in markets that are still flooded with foreclosures.

Closing costs are no fun, but a reality when getting a mortgage, even a mortgages for depression income families. If there'due south any chance the seller will help, you might every bit well ask.

Click here to bank check your abode ownership eligibility status.

How Lenders Decide Whether You're Approved

At present that we've reviewed your tools equally a depression-income home buyer, permit'due south swoop into the nuts of getting a mortgage. These are rules that apply to anyone, with any income, getting any type of mortgage.

Credit. This is the one expanse of the loan application where you can really smoothen fifty-fifty if you lot have a low income. A lender wants to know you've been faithful in smaller responsibilities before handing you a big responsibility. It doesn't matter that your auto loans, credit carte limits, and such are smaller than those of higher-income borrowers.

The only affair that matters is that you've handled the credit – whatever size – responsibly.

A keen credit score tin raise the dollar amount you authorize for. If you don't have a bang-up credit score, you may desire to work on that first before continuing your homeownership journeying. As a low-income borrower, yous need to accept all other aspects of your mortgage awarding in top shape to get the best dwelling available. Check out our articles and videos on credit here.

Employment.The lender will want to run across that you have steady employment, fifty-fifty if income from that employment is low at the moment.

It looks much better on a mortgage application if y'all've had i task over the past 2+ years rather than many jobs. The lender wants to know that you lot tin hold down a chore. It will be your means of repaying your mortgage, after all.

If you have had a few jobs over the past few years, work up a smashing letter explaining why you changed jobs. Did downsizing force you to change jobs? Too, necktie each employment experience together, stating how each one relates to the other. A long fourth dimension in the aforementioned line of work looks much better than a long history of unrelated jobs.

Debt vs. Income.This is a big 1. This could make the difference between you owning a habitation and continuing to rent.

The lender will look at how much debt you have compared to your income. Since your income is depression, you lot want your debt payments to be low equally well.

Here's why: y'all are capped at using almost 45% of your gross income for your entire housing costs plus whatever monthly debt. Hither's an example:

$3,000 gross monthly income

45% = $1,350.

- $200 car payment

- $250 student loan payment

- $50 minimum credit card payments

That's $850 per calendar month left for principle, interest, property taxes, HOA ante, and homeowners insurance.

But if you had just $50 per calendar month in credit card bills and no other debt, yous would have upward to $1,300 available for a house payment. That a $100,000 increase in your buying power considering of $450 less in monthly debt.

In the months and years before ownership a home, brand a plan to pay off debts.

Down Payment.Information technology's tough to save money. On a tight budget, information technology's hard plenty to put nutrient on the table. Luckily at that place are home loans for low-income families. Many options don't require a down payment. I go over these programs in the "Tool Belt" section beneath.

Even so, the lender volition want to see that you can salvage money. So even if it'due south only $25 per month, meet what expenses you tin can cut out of your budget to put toward a savings business relationship.

Property.The lender checks out the property to brand sure information technology meets minimum requirements. You might exist tempted to look into a fixer-upper to get a lower purchase toll that fits within your budget. That'due south fine, just keep in mind that loan approval is tough with a beat-upwardly home.

Get Pre-Approved Before Looking for a Home

Because you're looking for a low-income domicile loan, it'south very likely that you could be close to maximum debt ratio limits. That'southward why it's a good idea to get a pre-approval from a lender.

The pre-blessing will tell you your maximum purchase price. Always know this magical number before looking at homes. There'southward nada worse than falling in love with a home that'south out of your price range.

Click here to see if you authorize for a abode loan.

Final Words Most Low-Income Home Loans

At that place are tons of options out there for low-income home buyers. It'due south only a matter of finding the right one.

Go on at information technology. Just because you are denied the starting time time doesn't hateful yous can't re-apply after y'all've cleaned up your credit, received a raise, or paid off debt.

With some perseverance and cognition, you'll be in your own domicile before you know information technology.

Click here to bank check your eligibility for a low-income home buying programme.

cashwelllouns1959.blogspot.com

Source: https://mymortgageinsider.com/low-income-home-loans-and-mortgage-programs/

0 Response to "Best Way to Finance a House for Low Income Families"

Postar um comentário